The monetary bureaucrats in the United States, Europe and Japan have delivered ultra-low interest rates. When combined with the exchange-rate regimes in most Asian countries, these low interest rate policies have created a hotmoney cocktail. In May, the United Nations Economic and Social Commission for Asia and the Pacific recommended the imposition of exchange controls to curb inflows of hot money into the region. On June 13 and 16, South Korea and Indonesia, respectively, took the U.N. bait and introduced new exchange controls.

To understand the causes of hot money flows, we must examine the basic types of exchange-rate regimes. Let’s take a look (see accompanying chart).

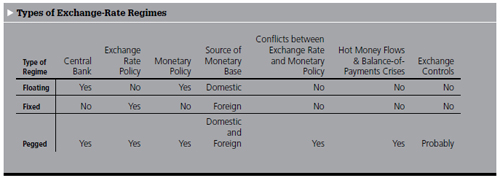

Free-Market Regimes

Although floating and fixed rates appear dissimilar, they are members of the same free-market family. Both operate without exchange controls and are free-market mechanisms for balance-of-payments adjustments. With a floating rate, a central bank sets a monetary policy but has no exchange rate policy — the exchange rate is on autopilot. In consequence, the monetary base is determined domestically by a central bank. With a fixed rate there are two possibilities: either a currency board sets the exchange rate, but has no monetary policy — the money supply is on autopilot — or a country is “dollarized” and uses a foreign currency as its own.

Under a fixed-rate regime, a country’s monetary base is determined by the balance of payments, moving in a one-to-one correspondence with changes in its foreign reserves. With both of these free-market exchange rate mechanisms, there cannot be conflicts between monetary and exchange rate policies, and balance-of-payments crises (and hot-money flows) cannot rear their ugly heads. Floating- and fixed-rate regimes are inherently equilibrium systems in which market forces act to automatically rebalance financial flows and avert balance-of-payments crises and hot money flows.

Pegged Rates Invite Trouble

Most economists use “fixed” and “pegged” as interchangeable or nearly interchangeable terms for exchange rates. While these two types are superficially similar, they are fundamentally very different types of exchange-rate arrangements. Pegged-rate systems are those where the monetary authority is aiming for more than one target at a time. Indeed, pegged rates require a central bank to manage both the exchange rate and monetary policy.

With a pegged rate, the monetary base contains both domestic and foreign components. Pegged systems — which include pegged, but adjustable rates, crawling pegs, and managed floating rates — go hand-in-glove with hot money flows. These systems often employ exchange controls and are not free-market mechanisms for international balance-of-payments adjustments. Pegged exchange rates are inherently disequilibrium systems, lacking an automatic mechanism to produce balance-of-payments adjustments.

Unlike floating and fixed rates, pegged rates invariably result in conflicts between monetary and exchange rate policies. For example, when capital inflows become “excessive” under a pegged system, a central bank often attempts to sterilize the ensuing increase in the foreign component of the monetary base by selling bonds, reducing the domestic component of the base. And when outflows become “excessive,” a central bank attempts to offset the decrease in the foreign component of the base by buying bonds, increasing the domestic component of the monetary base.

Balance-of-payments crises erupt as a central bank begins to offset more and more of the reduction in the foreign component of the monetary base with domestically created base money. When this occurs, it is only a matter of time before currency speculators spot the contradictions between exchange rate and monetary policies (as they did in the Asian financial crisis of 1997—98) and force a devaluation, the imposition of exchange controls, or both.

Hot Money and Exchange Controls

Hot money flows are principally associated with pegged exchange rates. Many analysts have misdiagnosed the so-called hot money problem because they have failed to appreciate this all-important linkage. In consequence, they have prescribed exchange controls as a cure-all to cool off the hot money. That prescription treats the symptoms. It fails to treat the disease: pegged exchange rates. Until pegged rates are abandoned, there will be volatile hot money flows and calls to cool the hot money with exchange controls.

Currency convertibility is a simple concept. It means residents and nonresidents are free to exchange domestic currency for foreign currency. However, there are many degrees of convertibility, with each denoting the extent to which governments impose controls on the exchange and use of currency.

The pedigree of exchange controls can be traced back to Plato, the father of statism. Inspired by Lycurgus of Sparta, Plato embraced the idea of an inconvertible currency as a means to preserve the autonomy of the state from outside interference. It is no wonder that the leadership in Beijing finds the idea of an inconvertible yuan so attractive.

The temptation to turn to exchange controls in the face of disruptions caused by hot money flows is hardly new. Tsar Nicholas II first pioneered limitations on convertibility in modern times, ordering the State Bank of Russia to introduce, in 1905—06, a limited form of exchange control to discourage speculative purchases of foreign exchange. The bank did so by refusing to sell foreign exchange, except where it could be shown that it was required to buy imported goods. Otherwise, foreign exchange was limited to 50,000 German marks per person. The Tsar’s rationale for exchange controls was that of limiting hot money flows, so that foreign reserves and the exchange rate could be maintained. The more things change, the more they remain the same.

Before more politicians come under the spell of exchange controls, they should reflect on the following passage from Nobel laureate Friedrich Hayek’s 1944 classic, The Road to Serfdom:

The extent of the control over all life that economic control confers is nowhere better illustrated than in the field of foreign exchanges. Nothing would at first seem to affect private life less than a state control of the dealings in foreign exchange, and most people will regard its introduction with complete indifference. Yet the experience of most Continental countries has taught thoughtful people to regard this step as the decisive advance on the path to totalitarianism and the suppression of individual liberty. It is, in fact, the complete delivery of the individual to the tyranny of the state, the final suppression of all means of escape — not merely for the rich but for everybody.

Hayek’s message about convertibility has regrettably been overlooked by many contemporary economists. Exchange controls are nothing more than a ring fence within which governments can expropriate their subjects’ property. Open exchange and capital markets, in fact, protect the individual from exactions, because governments must reckon with the possibility of capital flight.

From this it follows that the imposition of exchange controls leads to an instantaneous reduction in the wealth of the country, because all assets decline in value. To see why, it is important to understand how assets are priced.

The value of any asset is the sum of the expected future installments of income it generates discounted to the present value. For example, the price of a stock represents the value to the investor now of his share of the company’s future cash flows, whether issued as dividends or reinvested. The present value of future income is calculated using an appropriate interest rate that is adjusted for the various risks that the income may not materialize.

When convertibility is restricted, risk increases, because property is held hostage and is subject to a potential ransom through expropriation. As a result, the risk-adjusted interest rate employed to value assets is higher than it would be with full convertibility. Investors are willing to pay less for each dollar of prospective income and the value of property is less than it would be with full convertibility.

This result, incidentally, is the case even when convertibility is allowed for profit remittances. With less than full convertibility, there is still a danger the government will confiscate property without compensation.

That explains why foreign investors are less willing to invest new money in a country with such controls, even with guarantees on profit remittances.

Investors become justifiably nervous when they expect that a government may impose exchange controls. Settled money becomes “hot” and capital flight occurs. Asset owners liquidate their property and get out while the getting is good. Contrary to popular wisdom, restrictions on convertibility do not retard capital flight, they promote it.

Full convertibility is the only guarantee that protects people’s right to what belongs to them. Even if governments are not compelled by arguments on the grounds of freedom, the prospect of seeing every asset in the country suddenly lose value as a result of exchange controls should give policymakers pause.

This brings us to China — a country with a plethora of exchange controls and an inconvertible currency. Beijing should adopt a fixed exchangerate regime. This would force Beijing to dump exchange controls and make the yuan fully convertible. Such a “Big Bang” would muzzle the China-bashers and put Beijing in the driver’s seat. After all, China would then have a stable, freemarket exchange-rate regime.

Author Steve H. Hanke

0 responses on "The Dead Hand of Exchange Controls"