The course of the us dollar over the past few years has been anything but smooth. From November 2002 until mid-July 2008, the greenback lost 37% of its value against the euro. This period of dollar weakness began when Ben S. Bernanke, then a Federal Reserve governor and now the chairman, persuaded Alan Greenspan, then chairman, that the US was in the grip of deflation.

In consequence, the Fed pushed down on the monetary accelerator. By July 2003 the Fed funds rate had been squeezed down to 1%, where it stayed for a year. This artificially low interest rate set off the mother of all liquidity cycles. Artificially low interest rates encouraged investors to take undue risks, chasing the slightest available yields. To make the most of tiny yields, leverage became the flavor of the day.

Carry trades — borrowing in low-yield currencies, such as the dollar, and investing in higher-yield ones — also became popular. Borrow, borrow, borrow. The resulting mountain of debt had to collapse, and it did. From mid-July 2008 until the end of November 2008, the dollar switched course, surging against the euro with a 28% appreciation. It was during this period that the asset bubbles created earlier started to pop. In consequence, the demand for dollars soared as carry trades were unwound and investors scrambled to find shelter from the storm.

As the skies began to clear in December 2008, the dollar reversed course again. Indeed, in the December 2008-June 2009 period, the greenback lost 11% against the euro. The volatile dollar has resulted, among other things, in a wild roller-coaster ride for commodity prices.

The dollar-commodity price linkage exists because most commodities are priced and invoiced in dollars. In consequence, even if a commodity’s supply and demand fundamentals don’t budge, the nominal price of a commodity will change as the value of the dollar changes. If the dollar’s value sinks, the nominal price of a commodity will rise and vice versa.

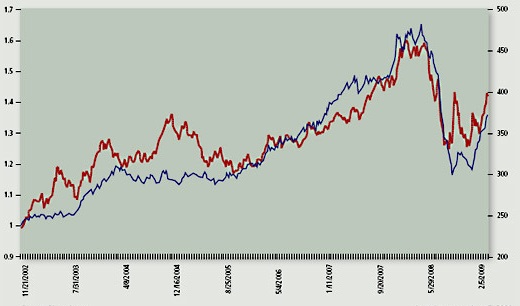

The accompanying chart traces the movements in the dollar-euro rate and the path taken by the Commodity Research Bureau’s index of 22 commodities. As the dollar lost ground, commodity prices took off. Indeed, the weak dollar accounted for the bulk of the commodity price increases during the great commodity bull market which ended in July 2008.

Thin dotted line: USD/Euro (left axis)

Thick solid line: CRB all US commodities Spot Index (right axis)

Contribution to oil price

For example, crude oil traded on the spot market at $19.84 per barrel on 28 December 2001. Adjusted for the change in the value of the dollar, assuming no changes in crude oil fundamentals, the nominal price of crude oil would have been $81.45 per barrel on 11 July 2008. In fact, the price on 11 July 2008 was $145.66 per barrel.

Therefore, the drop in the value of the dollar contributed 51% of the price increase from the end of 2001 to mid-July 2008 and positive fundamentals (changes in supply and demand) contributed 49% of the increase in crude oil price.

The volatile dollar, which serves as the world’s premier currency (see accompanying chart), has opened the door for complaints. For one thing, commodity producers and consumers don’t like the unstable commodity prices that accompany a volatile dollar.

Composition of world allocated foreign exchange reserves

It’s no surprise that both Russia and China have raised the specter of replacing the dollar as the world’s reserve currency. Moscow and Beijing have suggested using the International Monetary Fund’s Special Drawing Rights (SDR) instead of the greenback.

The SDR was created in 1969. At present, it is an artificial metric which consists of 0.6 US dollars, 0.4 euros, 18.4 yen and 0.09 British pounds. Its value fluctuates with exchange rates. Today, one SDR is equal to 1.54 US dollars. The SDR is not a tangible medium of exchange or a claim on one. It’s simply an accounting metric the IMF uses to balance its books. It has no real commercial application.

This led the Brazilian economist Prof. Alexandre Kafka, who served as an executive director of the IMF for over three decades, to lament that the IMF’s “basket currency” had become a “basket case.” Until a few months ago, it appeared that a 40-year experiment had ended in failure. Or has it?

While the dollar is not going to be displaced by the SDR as the world’s reserve currency anytime soon, the stars seem to be aligned for a full-blown debate about the SDR’s future role. Perhaps another chapter in the long-running SDR saga is about to open. As a precursor, the April 2009 Group of Twenty meeting in London concluded with a pledge to increase the IMF’s SDR allocation by $250 billion. That is almost an eight-fold increase over the current stock of $32 billion.

In addition, the Russian bear is showing its teeth and China is gaining ground in the economic power game (see accompanying table). Both are beating the drums for wider use of the SDR.

Share of World GDP (%)

")

Source: The Conference Board and Groningen Growth and Development Centre, Total Economy Database, January 2009 (http://www.conference-board.org/economics/) and author’s calculations. Note: The GDP numbers are converted at Geary Khamis

PPPs to 1990 USD. N/A: Not available

And that’s not all. The current IMF managing director is Dominique Strauss-Kahn, a French socialist and a strong SDR advocate. Interestingly, the last time the SDR received a big boost was in the late 1970s, when the IMF’s managing director was the distinguished Frenchman Jacques de Larosière.

Dollar hegemony has never been a Paris favorite. With Moscow and Beijing joining in, the SDR promises to become a favorite topic of the chattering classes, if not more.

Author Steve H. Hanke

0 responses on "The Volatile Dollar"