The world is in the midst of a classic boom-bust cycle. These cycles start when central banks push interest rates below where they would have been set in a free market. The artificially low interest rates set off a credit boom in which businesses and households take on more debt and leverage up.

In consequence, the ratio of debt to assets (or equity or income) increases and asset markets boom. When leverage and debt reach unsustainable levels, the boom ends and a bust ensues. As businesses and households sell assets to deleverage and reduce their debt levels, booming asset markets shift into reverse.

At present, balance sheet repair dominates. Regardless of how low the Fed pushes interest rates, businesses and households are not inclined to take on more debt. Instead, they want to reduce their leverage and debt burdens.

This process will come to a halt, but only after asset prices reach bargain basement levels and leverage ratios become sustainable.

The current deflationary forces are strong. Since July, the Fed has been attempting to counter them. Indeed, the Fed’s balance sheet has more than doubled in less than five months (see accompanying chart) but this has not been enough to stabilize the credit system.

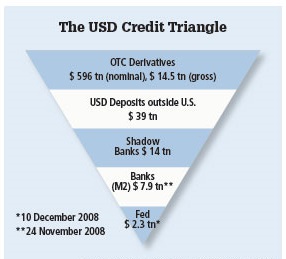

To better understand the forces at play and the rough magnitudes involved, we use a credit triangle. The triangle’s architect is John Greenwood. Recall that he was also the architect of Hong Kong’s modern currency board system.

For those who are interested in Hong Kong’s monetary setup, the standard reference is Greenwood’s book, Hong Kong’s Link to the US Dollar: Origins and Evolution, Hong Kong University Press, 2008.

The credit triangle depicts a modern fractional reserve banking system – one in which a small quantity of reserves (capital) is multiplied into a much larger volume of loans and deposits.

At the tip of the triangle is the Fed. It provides reserves to banks and the non-bank public. This so-called high-powered money is multiplied into $7.9 trillion of deposit liabilities held by traditional banks in the US. These banks are represented in the layer directly above the Fed. The deposits of firms and individuals at these banks represent money, as measured by M2.

Many people think the credit story ends here. But to understand the boom-bust cycle, we must include non-bank credit, as well as bank credit.

Shadow banks represent the next layer in the triangle. These include investment banks, mortgage finance companies, private equity pools, structured investment vehicles, etc. They issue credits that total $14 trillion.

These shadow banks rely on deposits held at banks for their reserves. Shadow banks have less capital relative to assets (higher leverage) than traditional banks. In addition, they are not subject to the same level of prudential regulation as traditional banks.

Banks and other financial institutions outside the US accept US dollar deposits, issue dollar-denominated debt and make dollar- denominated loans and investments. This segment does not hold reserves at the Fed and is more leveraged than its onshore counterparts.

At $39 trillion, it is large and important. Indeed, it plays a critical role in supplying credit (letters of credit) to those who engage in international trade.

The top layer of the triangle represents over-the-counter derivatives. They have a nominal value of $596 trillion and a gross value (the replacement cost of all outstanding contracts if they were settled) of $14.5 trillion.

The credit triangle is a top-heavy structure. At each higher level in the triangle, there is more leverage (less capital to assets) and more credit. When a bust arrives, banks and other financial institutions scramble to reduce their exposure to risky assets and the layers of the triangle contract, with the upper layers contracting relatively more than the lower ones.

Even though the Fed has engaged in a massive expansion of its balance sheet, the weight of the deleveraging and compression of the upper layers of the credit triangle have more than offset the Fed’s moves.

Until the deleveraging process runs its course, bet on the Fed to continue the rapid expansion of its balance sheet. Then, to avoid a burst of inflation, the Fed will have to rapidly deleverage its own balance sheet. This contraction promises to be more difficult than the current expansion.

Author Steve H. Hanke

0 responses on "The Credit Triangle"